ThreeSixty Research Market Update May 2014

APRIL MARKET PERFORMANCE

The Pulse

|

|

Global economies

Global growth is around longer-term trend and further uplift is expected in Q2, for the remainder of 2014 and into 2015.

The April 2014 International Monetary Fund’s World Economic Outlook, outlined a broadening and strengthening of global economic activity in 2014 and 2015.

The US is showing early positive signs of a recovery from the flat growth in Q1.

The Eurozone is showing improving individual country growth, expanding into countries outside of Germany and France.

China’s economic growth has been slowing over Q1 but showed signs in April of stabilising. People’s Bank of China has considerable policy flexibility with inflation subdued. However, economic rebalancing will continue to be challenging.

Japanese growth in April was slower but this was expected post the introduction of the new sales tax.

US

Over in the US, Q1 GDP came in as expected at an annual rate of 0.1%. This was the slowest growth since the Q4 of 2012.

However, a rebound is under way. April manufacturing data rose at its fastest pace for three years. New orders, robust output growth and greater confidence about the business outlook contributed to a solid upturn in manufacturing employment, rising for 10 consecutive months.

Consumer spending, which accounts for more than two-thirds of US economic activity, increased at 3% in March, and represented the largest gain in more than four and a half years. Spending on services grew at its quickest pace since the Q2 of 2000, with healthcare contributing 1.1% to GDP growth. Spending on durable goods rose 2.7%.

Overall, employment growth improved in April – with unemployment falling to 6.3%, down from 6.7% in March.

Inflation remains benign at +1.1% yoy in March well below the Federal target of 2%. This provides considerable pricing policy flexibility, allowing the Government to keep cash rates near zero for an extended period. Rates are not expected to move higher until sometime well into 2015.

Europe

In April, business activity in the Eurozone economy accelerated at its fastest pace for almost three years. This has led to job creation across the region. The Eurozone Purchasing Managers’ Index (PMI) data has been growing above trend for the past 10 consecutive months.

Interestingly, April new orders grew at their fastest pace since May 2011. Employment growth was the largest since September 2011. However, rates of job creation in both manufacturing and services remain at only modest levels.

German economic growth remains the standout across the Eurozone. Growth in new business provided the conduit for German corporates to increase employment at a stronger rate.

France also had its second consecutive month of increased output and the services sector continued to gain momentum.

Other Eurozone countries have also continued their recovery across both manufacturing and services sectors, with their best growth rate since early 2011. Employment has also increased for the first time since May 2011.

Adding to the positive news, the Eurozone PMI improvement is indicating that Q2 GDP is expected to rise by 0.5% and will build on the Q1 2014 uplift of 0.4%.

The concern that remains is that of deflationary pressures. Inflation across the 18-country Eurozone rose 0.7% in April. The European Central Bank is quite ready to provide further stimulus.

China

Across in China, their Q1 annualised GDP came in at 7.4% (down from 7.7% at 31 December 2013). The Government is forecasting 7.5% GDP for 2014.

China’s Manufacturing PMI stabilised in April. Domestic demand showed a mild improvement and deflationary pressures eased, but downside risks to growth are still evident as both new export orders and employment contracted.

The State Council has outlined a spending package on railways and housing, plus tax relief to support growth. The central bank also lowered the reserve-requirement ratio for some rural banks by as much as 2%. While the initial impact from these measures will likely be limited, they signal readiness to do more if necessary.

China’s April inflation remains subdued at 1.8%, well below the 3.5% target rate. This continues to offer policy flexibility if required to continue to stimulate the economy.

Asia region

The headline Japan PMI fell to 49.4 in April from 53.9 in March, the first sub-50 reading in 14 months. As expected, the increase in the sales tax negatively impacted manufacturing companies. Output and new orders both declined.

However, the labour market seems to be in good order. Payroll numbers in April increased faster than in March and growth in employment was the sharpest since February 2007. Japanese manufacturers have experienced nine consecutive months of growth in employment. It’s uncertain whether the increase in the sales tax will continue to have a negative impact on Japanese manufacturing activity in future months.

Inflation continues to be buoyed by the 2013 quantitative easing package. Japanese inflation in March was running at 1.61% yoy.

Australia

The Federal Government released the findings of the National Commission of Audit. It contains 86 recommendations aimed at saving the budget $70 billion annually.

The country will be waiting to hear what parts of the Commission’s report will be embraced by the Federal Government when it releases its Budget on 13 May – expected to be one of constrained expenditure.

Some of the key recommendations include:

-

raising the pension age to 70 by 2053

-

including the family home in a new means test from 2027

-

raising the superannuation preservation age to 62 by 2027

-

slowing the roll-out of the national disability insurance scheme

-

$15 co-payment to visit the doctor and to access Medicare services

-

requiring wealthy Australians to have private health insurance

-

increasing co-payments for taxpayer-funded medicines, and

-

opening the pharmacy sector to competition, such as supermarkets.

House price growth across the eight capital cities cooled somewhat in April. Although Sydney increased 0.5% in April, representing a 16.7% increase for the rolling year, there are signs price increases are slowing down. Melbourne prices eased 0.5%, and represent an 11.6% increase on a rolling annual basis.

Business credit continued to grind higher, up 0.2% in March. Although encouraging, additional growth would signal a recovery in business investment and employment growth.

Housing credit growth was up 0.5% in March (5.6% yoy) – investor lending at 7.9% and owner-occupied at 4.9% yoy. But despite the house price boom, the past two months have seen housing credit slow.

Q1 inflation data of 2.9% surprised the market and remains within the 2-3% target range. This number is expected to allow the RBA to remain on hold as regards the cash rate for some period of time.

Equity markets

|

Australian Equities

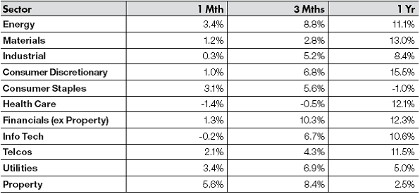

After a flat performance in March, the Australian equity market experienced a strong month in April. The S&P/ASX 300 Accumulation Index had an excellent month, increasing by 1.68%. Property, Energy, Utilities and Consumer Staples sectors all had a standout month.

The S&P/ASX All Ordinaries Index had a strong April, posting a return of 1.41%.

For the 12 months to 30 April 2014, the S&P/ASX 300 Accumulation Index posted a reasonable gain of 10.14%; while the large market caps, comprising of the S&P/ASX 50 Accumulation Index, performed even better, returning 10.65%.

The A-REIT sector was the clear standout in April, up 5.6%, while the Energy and Utilities sectors both returned 3.4%. Consumer Staples also had a strong month, up 3.1%.

The Healthcare, Information Technology and Industrial sectors were the worst performing sectors in April. Healthcare and Information Technology declined 1.4% and 0.2% respectively, while the Industrial sector was only up 0.3%.

Big movers this month

Going up: Property +5.6%

Going down: Healthcare -1.4%

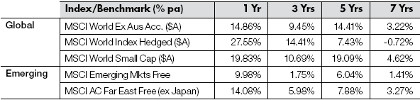

Global equities

The MSCI World (ex-Australia) Accumulation Index had an improved performance in April, up 0.49% after a flat performance in March.

The US Dow Jones Index was up 0.75% and joined in the global uptrend in equity markets. The S&P 500 Index was up 0.62%.

The Nikkei was one of the major underperformers in April, down 3.53%. Although having had a strong 2013, the equity market is now up only 3.2% on a rolling 12 months basis.

Europe has now started to outperform Asia. France was a standout, up 2.18% in April and up 16.35% on a 12 month basis. Germany was 0.5% but has been a strong performer over 12 months, up 21.35%.

UK had a strong performance in April, up 2.75% but only up 5.44% on a 12 month basis.

Most other global markets were up in April, offsetting the largely negative returns in March.

Property

In April, the S&P/ASX 300 A-REIT Accumulation Index posted a strong 5.63% gain, once again outperforming the broader S&P/ASX 300 Accumulation Index.

On a 12 month rolling basis, property continues to underperform compared to the ASX 300 Accumulation Index. In fact, the 12 month return for the S&P/ASX 300 A-REIT Price Index is down 3.18% while the S&P/ASX 300 A-REIT Accumulation Index is up 2.51% for the year to April, compared to the All Ordinaries’ Accumulation Index rise of 10.43% for the same period.

Over the 1 year period, Australian A-REITs have outperformed global property. However, over the long-term, global property has continued to outperform the Australian listed property sector. Global property, as represented by the FTSE EPRA/ NAREIT Index was up 0.55% over the rolling one year period.

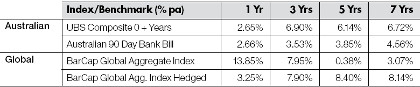

Fixed interest

US 10-year bond yields were lower in April, closing the month at 2.65% (down 3.96%). Australian 10-year bond yields were also down and closed the month at 3.95% (down 4.49%).

Australian bonds were relatively subdued during April. For the month, the UBS Composite Bond All Maturities Index was down 1.24%.

Global bonds, as measured by the Barclays Capital Global Aggregate Index, were mixed against the Australian index. The unhedged index posted a gain of 1.16% for April, while the hedged equivalent had a positive return of 0.90%.

On a 12 month basis, Australian bonds returned 2.65%, but underperformed relative to unhedged global bonds that were up 13.85%. Hedged global bonds were also higher returning 3.25%.

Australian dollar

In April, the Australian Dollar (AUD) was up relative to most major currencies. The AUD increased 0.41% against the US Dollar (USD) to finish the month at 92.88 US cents. Over the past 12 months the AUD has declined significantly against the USD, down 10.46%.

The largest AUD decline in April was against the Euro (down 0.42%). On a 12 month basis, the AUD is down -14.99%.

Against the Japanese Yen, the AUD was down 0.41% during April, but is down 6.01% for the 12 month period. Against the British pound the AUD was down -0.98%. The largest 12 month fall in the AUD was relative to the British pound (down -17.57%).

The information contained in this Market Update is current as at 2/5/2014 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty Research, registered office 150-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.