ThreeSixty Research Market Update June 2014

MAY MARKET PERFORMANCE

The Pulse

|

|

Global economies

There are now signs of stabilisation in growth across the US and China. The US Federal Government proceeded with another US$10 billion cut to its monthly quantitative easing programme (currently US$45 billion), while the Chinese industrial activity gained some support from a series of targeted stimulus policies.

In light of stronger expectation for Q1 due to a pick-up in exports, NAB has revised its Australian GDP forecasts up for FY14 and FY15. NAB has also changed its rate call and now expects that we’re at the bottom of the interest rate cycle. Having said this, there are not great expectations of interest rates rises in the short term priced into markets either.

US

Taking a closer look at the US, Q1 GDP has been revised down. The advance estimate for Q1 GDP growth was initially 0.1% quarter on quarter (annualised rate). However, this has now been revised down further to show negative growth of -1.0%.

Several factors appear to be behind the sharp slowdown. These include:

-

a correction to strong growth in the second half of 2013, as inventory accumulation slowed and the strong Q4 net export performance was unwound, and

-

equipment investment also declining after spiking towards the end of 2013.

In positive news, the labour market continues to improve. April saw a large fall in the unemployment rate, while other labour market indicators are also improving but more slowly. Wages growth remains muted.

Private consumption growth held up in Q1. However, most categories of consumption were weak and the strong overall result was largely due to high rates of power and health care consumption growth. In contrast, business fixed investment declined and residential investment went backwards for the second consecutive quarter.

Overall, a deceleration in growth was not a surprise, as the harsh winter and slower inventory accumulation were expected to take a toll. The bigger issue now is whether the data over the course of Q1 and into Q2 are consistent with the view that it was a one-off and the broader recovery is still on track.

At this stage, the indicators are consistent with this view and point to a bounce back in economic growth in Q2. Partial indicators of consumption, business investment, exports and employment have strengthened over the recent months, with housing the main area still showing weakness.

Europe

Over in the Eurozone, Q4 GDP was better than expected with growth increasing to 0.3% from just 0.1% quarter on quarter in Q3 2013. This growth confirms the recovery is continuing, albeit slowly. It’s the first time that all four major Eurozone economies recorded positive growth since 2011.

Purchasing Managers’ Index (PMI) data also shows that the Eurozone is continuing to grow in 2014.

Eurozone headline inflation has fallen sharply from 3% yoy in late 2011 to 0.7% yoy in April 2014. This is well below the European Central Bank’s (ECB) 2% inflation target. Although some of this is due to declining food and energy inflation, core inflation has also declined.

A key source of Eurozone disinflation is spare capacity built up during the GFC, which the International Monetary Fund estimates could take five more years to use up. This increases the likelihood that the ECB will need to lower interest rates again before the year is out.

China

In China partial economic indicators continue to highlight softening trends, evident since the latter part of 2013. These trends remain in line with NAB expectations, and as such, NAB forecasts for Chinese economic growth are unchanged at 7.3% in 2014 (before slowing to 7% in 2015).

Recent commentary by both China’s President and the Governor of the People’s Bank of China appears to indicate an acceptance of slower growth trends – with Governor Zhou Xiaochuan commenting that the Government would ‘fine tune’ its policy to counter economic cycles, but not use any large-scale stimulus to boost the economy (China Daily).

Industrial production was marginally softer in April, increasing by 8.7% yoy (compared with 8.8% in March). Although production levels are slightly above the recent lows of February, output remains comparatively soft, around the weakest levels since China recovered from the GFC.

The various manufacturing PMI surveys highlight mixed conditions in the industrial sector. The official National Bureau of Statistics PMI (covering larger firms) was slightly improved by 0.1 point in April at 50.4 points, while the HSBC Markit PMI continued to weaken, down 0.2 points to 48.1 points.

Asia region

For the Asian region Q1 GDP results there was a mix of outcomes.

Indonesia experienced their slowest growth rate in 4 years, while across in the Philippines GDP growth was the slowest in 2 years. This was an unexpected result mainly attributed to the impact of last year's super typhoon.

On the flip side, South Korea’s GDP growth was firm, while Taiwan’s GDP growth was the quickest in over a year.

In between these two outcomes were Singapore and Hong Kong, which both reported slowing GDP.

In Japan, the key news that came out in May was that retail sales fell 4.4% in April yoy. This was the result of an increase in the country's sales tax. Japan raised the tax rate from 5% to 8% on 1 April - the first increase in 17 years by Japanese policy makers to increase inflation to try and stop consumers from delaying consumption. It is thought that the drop in sales is only a temporary reaction to the increased tax and it is expected that sales will pick up in the future.

Australia

On home soil, the Commonwealth Government’s budget dominated the economic news in May. Love it or hate it, a tougher than usual budget was always on the cards. Consumer sentiment has plummeted in response to the budget and there are also likely implications for businesses.

According to NAB, cutting the company tax rate from 30% to 28.5% will benefit a considerable number of businesses. However, for the largest 300 businesses this cut is likely to be offset by the Paid Parental Leave Scheme levy. It’s also worth noting that the tax cut, the Paid Parental Leave Scheme and levy appear to be in government contingencies, suggesting some uncertainty about their implementation.

The infrastructure package is aimed at improving road, rail and air transport links, albeit heavily weighted towards roads. Improved freight movements and passenger transport should assist productivity and have some impact on wellbeing.

Treasurer Joe Hockey reiterated in his Budget speech that the “age of entitlement” is over, including for business. That said, businesses were spared the full weight of cuts recommended by the Commission of Audit.

On the positive side, there’s an increase of capital to the Export Finance and Insurance Corporation, and Export Market Development Grants, as well as the establishment of the Entrepreneurs Infrastructure programme. However, the cessation of some other industry assistance programmes could be detrimental to some businesses, while a cut of approximately $111.4 million to the CSIRO could detract from the agency’s ability to assist with industry enhancing innovation.

In non-budget news, building approvals fell 5.6% in April and represented the third consecutive month of declines (six within the past seven months). House price data has also slowed with consumer confidence waning.

Equity markets

|

Australian Equities

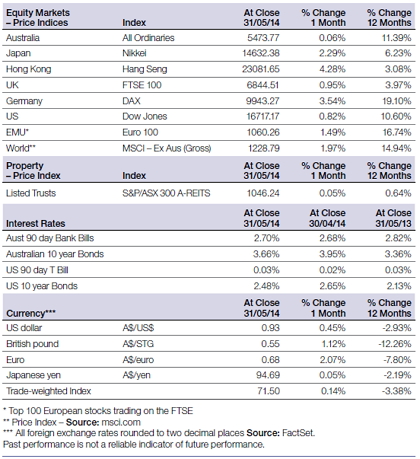

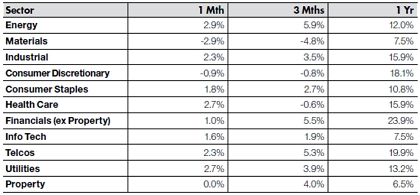

The S&P/ASX 300 Accumulation Index had a fairly average month in May, increasing by 0.65%, with Energy being the best performing sector returning 2.9%.

The S&P/ASX All Ordinaries Index had a flat May, posting a return of 0.1%.

For the 12 months to 31 May 2014, the S&P/ASX 300 Accumulation Index posted a solid gain of 16.12%; while the large market caps, comprising of the S&P/ASX 50 Accumulation Index, performed even better, returning 16.97%.

The Materials and Consumer Discretionary sectors were the worst performing sectors in May, declining 2.9% and 0.9% respectively. Energy, Health Care and Utilities were the best performing sectors. Overall, the performance of the sectors for the month was contained within a relatively narrow band of -2.9% to 2.9%.

Big movers this month

Going up: Energy +2.9%

Going down: Materials -2.9%

Global equities

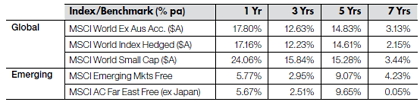

The MSCI World (ex-Australia) Accumulation Index posted a solid return in May, up 1.97%.

Apart from Australia, the US Dow Jones was the worst performing market returning 0.8% for the month. The best performing of the majors was the Hang Seng up 4.3%.

Over the 12 months to 31 May, the German DAX still leads the way returning 19.1%.

Overall, May was a good month for world markets, with all the majors up during May.

Property

In May, the S&P/ASX 300 A-REIT Accumulation Index posted a very small gain of 0.05%, underperforming the broader Australian market as measured by the S&P/ASX 300 Accumulation Index that returned 0.65%.

On a 12 month rolling basis, property continues to underperform compared to the ASX 300 Accumulation Index. In fact, the 12 month return for the S&P/ASX 300 A-REIT Accumulation Index is around 10% lower than the ASX 300 Accumulation Index.

Over the 1 year period, Global REITs have outperformed Australian REITs. Over the long-term, global property has continued to outperform the Australian listed property sector. Global property, as represented by the FTSE EPRA/ NAREIT Index was up 11.68% over the rolling one year period.

Fixed interest

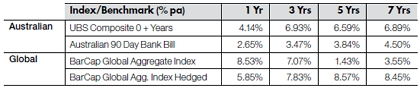

US 10-year bond yields were lower in May, closing the month at 2.48% (down from 2.65%). Australian 10-year bond yields were also down and closed the month at 3.66% (down from 3.95%).

Australian bonds rebounded after a poor April. For the month, the UBS Composite Bond All Maturities Index was up 1.37%.

Global bonds, as measured by the Barclays Capital Global Aggregate Index, posted positive returns for the month of May. The unhedged index posted a small gain of 0.14%, while the hedged equivalent had a solid positive return of 1.17%.

On a 12 month basis, Australian bonds returned 4.14%, but underperformed relative to unhedged global bonds that were up 8.53%. Hedged global bonds were also higher returning 5.85%.

Australian dollar

In May, the Australian Dollar (AUD) was up relative to the four major currencies. The AUD increased 0.45% against the US Dollar (USD) to finish the month at 93.07 US cents. Over the past 12 months the AUD has declined against the USD, down 2.93%.

The largest AUD gain in May was against the Euro (up 2.07%). On a 12 month basis, the AUD is down 7.80% against the Euro.

Against the Japanese Yen, the AUD was fairly flat in May, rising only 0.05%. Against the British pound the AUD was up 1.12%. The largest 12 month fall in the AUD was relative to the British pound (down 12.26%).

The information contained in this Market Update is current as at 2/6/2014 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty Research, registered office 150-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.