ThreeSixty Research Market Update October 2014

SEPTEMBER MARKET PERFORMANCE

The Pulse

|

|

Global economies

Despite geopolitical tensions, and weak European data, global economic growth continues at a moderate pace. The IMF recently lowered its global growth forecast for 2014 to 3.3% and 3.8% in 2015 and indicated that the Eurozone and Japan provide considerable headwinds.

It has been a volatile month for global equity markets, impacted by the ongoing geopolitical tensions in the Ukraine and the Middle East. The political protests in Hong Kong and growing concerns over the spread of the Ebola virus have also been of influence.

The US economy continues its upward trend, with Q2 GDP data increasing to 4.6%, from 4.2%. Fixed business investment was a key feature (with a 9.7% increase), and manufacturing data has continued to improve.

Chinese growth remained sluggish in September but has generally been in line with objectives. A weak property market continues to be a challenge in the short term.

Eurozone manufacturing data remains weak with inflation data at marginally lower levels. The European Central Bank (ECB) has provided stimulus to the lagging Eurozone economies, with further measures expected.

There has been continued improvement in Australian business and consumer confidence, albeit from low levels, with further momentum across the residential construction sector.

The RBA kept the cash rate at 2.5% in October and it is anticipated that interest rates will remain at this level well into 2015.

US

Over to the US, we have seen a stronger US dollar due to a continued increase in economic growth, the prospect of increased interest rates, the weakness in the Eurozone and Japan and the weakness in commodity prices.

The services sector continued to expand, with a rise in new business volumes. The private sector has been driven by weaker energy prices, with capital expenditures improving over recent months.

Stronger non-farm payrolls data resulted in the unemployment rate declining to 5.9%, from 6.1% in August. Job creation has increased significantly from August; however flat hourly earnings indicate there is little to no wage inflation.

The August CPI declined marginally with the annual core CPI at 1.7%.

The US Q3 2014 corporate earnings reporting season has commenced, with expectation that earnings will grow by 4.4% in Q3 yoy – largely due to the earnings growth in the Telcos, Materials, Healthcare and Financial sectors.

Expectations are that the Federal Reserve will scale back quantitative easing (QE3) in October. Federal Reserve officials stressed ‘patience’ in waiting to raise interest rates, concerned about weaker foreign economic growth and the stronger USD.

Europe

Heading over to Europe, economic data remains weak; impacted by the geopolitical tensions in the Middle East and the Ukraine.

The Markit UK Manufacturing PMI recorded its lowest level since April 2013. Growth in new orders slowed for a third straight month, largely due to the strength of the sterling and weak demand in Europe.

Germany and France recorded weaker manufacturing PMI data – a disappointment given these core Eurozone economies showed substantial growth earlier in the year.

An inadequate monetary policy easing has put increased pressure on the ECB to head off the threat of falling prices as annual inflation fell to 0.3% (from 0.4% in August). The unemployment rate across the Eurozone remained unchanged at 11.5%.

The rapid growth in the UK services sector eased slightly in September. Despite the slower economic conditions, the Bank of England has forecast that the British economy will grow by 3.5% this year, putting it on track to be the world's fastest-growing, major advanced economy.

China

Over in China, manufacturing growth stabilised in September.

It is anticipated that the Chinese government’s monetary and fiscal policies will remain accommodative until there is a more sustained recovery in economic activity.

The August core inflation at 2.0% yoy is significantly below the targeted 3.5%, with the likelihood that the government will undertake additional stimulus measures.

Manufacturing PMI data remained unchanged. The factory sector showed signs of stabilisation; however, the property sector remains a source of concern for the economy.

Interestingly, new export orders (a gauge of external demand) expanded to anear five year-high of 54.5, though domestic demand appeared soft.

Asia region

The Japanese economy continues its slow move forward, with an increase in manufacturing activity in Q3. To continue its growth trend, the government will need to assess consumer spending and wage growth before making any further increases to the sales tax again in 2015.

Core inflation eased to 3.1% in August from 3.3% in July. However, excluding the impact from the sales tax increase, the core CPI is only 1.3%, well below the 2% inflation target.

The continued weakness in the Japanese Yen and the impact on corporate earnings should provide considerable tailwinds for the Japanese equity market through 2015.

The Hong Kong economy has been slightly impacted by the tension between the Chinese government and student protestors over the directive given by Beijing for the Hong Kong elections in 2018.

Australia

Back home, the Australian economy enjoyed only moderate growth; adjusting to the decline in investment spending in the resources sector. The RBA expects that growth will remain slightly below trend in the short term.

Inflation is expected to be in line with the 2-3% target over the next two years. The RBA left the cash rate unchanged at 2.5% at its October meeting.

Monetary policy remains accommodative and interest rates remain low. The AUD declined in September, largely due to the strengthening US dollar – but still remains high by historical standards, particularly given the further declines in key commodity prices in recent months.

The job market appears optimistic, despite the unemployment rate increasing to 6.1% in September. The expectation is that the labour market is gradually improving and the official jobless rate will stabilise at just above 6% for the next few quarters before decreasing. The upward trend in job ads continues to suggest solid employment growth in coming quarters.

House price increases have become a concern for the RBA. Specific focus is on the investor market in Sydney and Melbourne where loan approvals are 90% higher than two years ago in NSW and 50% higher in Victoria. Interestingly, average clearance rates across Sydney and Melbourne remain at 78%.

The AiG Performance of Construction Index (PCI) was strong in September – a nine year high due to an increase in house and apartment construction. The industry is expected to continue this trend due to a growing pipeline of residential work.

Equity markets

|

Australian equities

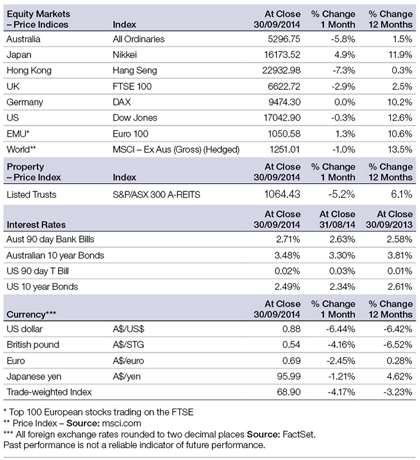

Following the recent positive gains, the S&P/ASX 300 Accumulation Index in September had an extremely disappointing month, declining by -5.37%. The Australian equity market was impacted by weaker commodity prices, the prospect of the completion of the dial down of the US Federal Reserve’s QE3, the prospect of a continued stronger US dollar and a weaker AUD, and global investors withdrawing funds from the higher yielding securities such as banks and A-REITs. The S&P/ASX 300 Industrials Accumulation Index was also disappointing in September, down -5.07%.

The broader S&P/ASX All Ordinaries Index was down -5.8% in September.

For the 12 months to 30 September 2014, the S&P/ASX 300 Accumulation Index posted a solid gain of 5.73%; while the large market caps, represented by the S&P/ASX 50 Accumulation Index, had a similar performance, returning 5.94%.

Interestingly, after strong performances across all sectors in August, sector performances were significantly lower in September. Financials (ex-A-REITs), Materials and Energy were the worst performing sectors, declining by -6.5%, -6.4% and -5.7%, respectively. Although all sectors declined, Healthcare was the best relative performer, down -0.1%.

Big movers this month

Going up: All sectors were down

Going Down: Financials (ex-A-REITs): -6.5%

Materials: -6.4%

Energy: -5.7%

Global equities

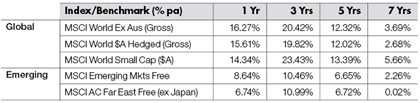

The MSCI World ex-Australia (unhedged) Index posted a strong positive return in September, up 4.3%. However, the MSCI World ex-Australia (hedged) Index was down -1%.

Continuing the recent pattern, the global indices recorded extremely divergent performance for the month.

The US S&P 500 Index was down -1.55% in September.

The Euro 100 Index was a strong relative equity market performer in September, up 1.3%.

The Japanese Nikkei Index was the standout performer across global markets in September, up 4.9%.

Over the 12 months to 30 September 2014, the S&P 500 Index was up 17.29%, the Dow Jones up 12.6%, the Nikkei up 11.9%, while the Hong Kong Hang Seng, the Australian All Ordinaries and the UK FTSE were up 0.3%, 1.5% and 2.5%, respectively.

Property

In September, the S&P/ASX 300 A-REIT Accumulation Index was down -5.2%, marginally outperforming the broader Australian market.

On a 12 month rolling basis, Australian listed property was up 12.28%, which significantly outperformed the ASX300 Accumulation Index.

Over the 3, 5 and 7 year periods, global REITs outperformed Australian REITs (A-REITs) and was only marginally lower compared to A-REITs over the 1 year. Global property, as represented by the FTSE EPRA/NAREIT Index, was up 12% over the rolling one year period.

Fixed interest

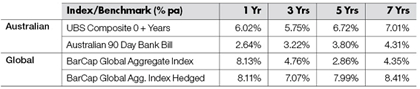

US 10-year bond yields were up 6.30% in September, closing the month at 2.49%. Australian 10-year bond yields were up 6% and closed the month at 3.48%.

For September, the UBS Composite Bond 0+YR Index was up 1.01%. On a 12 month basis, Australian bonds returned 6.02%, underperforming unhedged global bonds.

Global bonds (unhedged), as measured by the Barclays Capital Global Aggregate Index, posted positive returns for the one year period ended 30 September 2014, up 8.13%. The hedged index posted a strong one year gain of 8.11%.

Australian dollar

In September, the Australian Dollar (AUD) was down relative to all the major international currencies. The AUD declined by 6.3% against the US Dollar (USD), to finish the month at 87.5 US cents. Over the past 12 months, the AUD has declined by -6.17% against the USD.

The AUD declined against the Euro, down -2.57% in September. On a 12 month basis, the AUD was up 0.46% against the Euro.

Against the Japanese Yen, the AUD was down -1.32% in September. On a 12 month basis, the AUD was up 4.74% against the Yen.

Against the British pound, the AUD was down -4.07% in September. On a 12 month basis, the AUD was down -6.34% relative to the British pound.

The information contained in this Market Update is current as at 8/10/2014 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty Research, registered office 105-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.